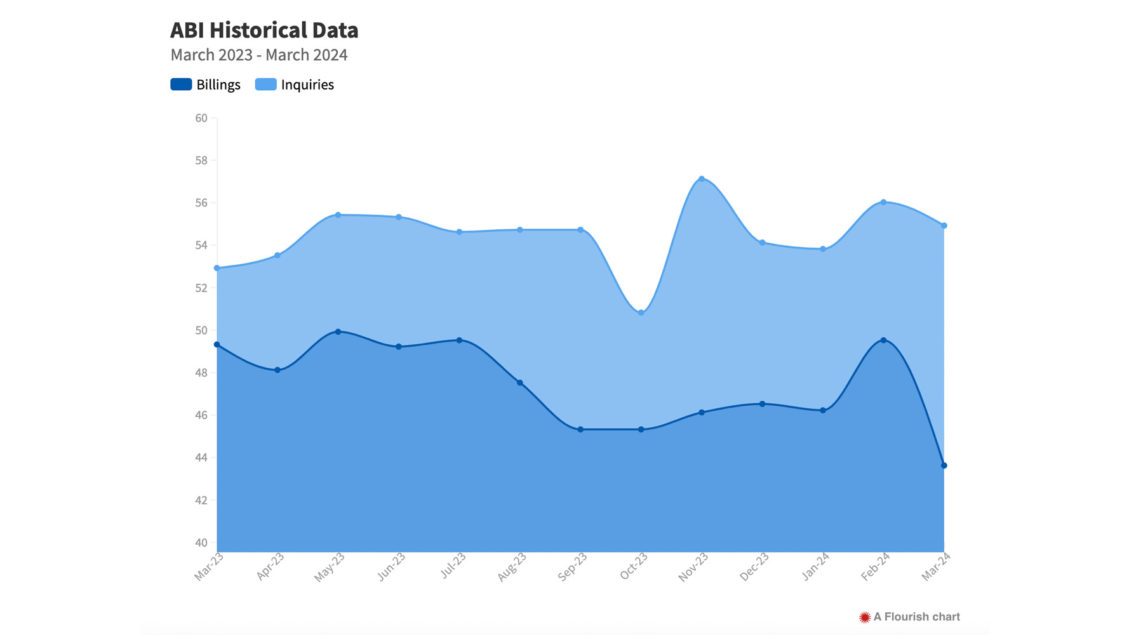

Architecture Firms Facing Persistent Business Challenges Amid Inflation and Supply Chain Disruptions

Architecture firms are facing challenging business conditions, as evidenced by the AIA/Deltek Architecture Billings Index (ABI) score of 43.6 for March. This marks the 14th consecutive month of decreasing billings,…

How Nelly Korda Became the World’s Top Teacher with Her Elite Full-Swing Wedges: 2 Key Tips for Success

Nelly Korda’s impressive golf game includes many aspects worth noting. At 25 years old, she made history by becoming the third LPGA Tour player to win five tournaments in a…

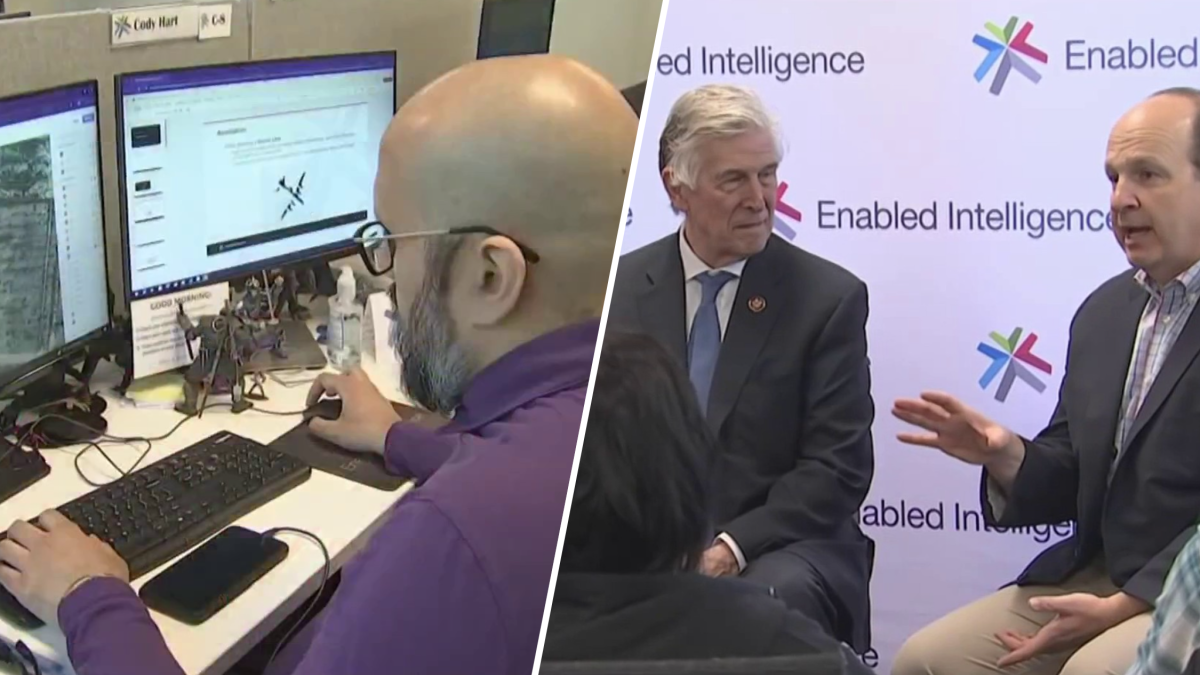

Neurodiverse individuals discover career opportunities in AI technology at a Northern Virginia company – NBC4 Washington报道

Data labeling or computer annotation may seem mundane, but for Cody Hart, who is neurodivergent, it adds value to his life. Hart expressed that working at Enabled Intelligence in Falls…

Three Arlington establishments recognized as top 250 sports bars in the U.S.

A recent ranking of the top 250 sports bars in the United States by betting site BetUS has identified three sports bars in Arlington, Virginia as being among the best…

Science With A Twist: Exploring the Personal Impact of Science on Local Residents through Storytelling at the Arizona Science Center.

The Arizona Science Center is hosting a special Science With A Twist event for guests 21 and over. This edition will feature a live show about how science has impacted…

FIT Together: A Six-Week Fitness Program Promoting Healthy Family Ties in Michigan City

A brand-new six-week fitness program, FIT-Together, is now open for registration at Franciscan Health Michigan City. This family-focused initiative aims to promote health and wellness among families with children aged…

The Rising Tide of Europe’s Economy Faces Challenges in Global Supply Chains: The Case of Iron and Steel Scrap

In recent years, Europe’s economy has shown signs of growth, as indicated by the recent strong Purchasing Managers’ Indices. The Eurozone saw a significant increase in April, with Germany’s service…

Biden Takes on Trump over Abortion Rights at Florida Campaign Event

At a campaign event in Florida, President Joe Biden criticized former President Donald Trump for his role in the overturning of abortion rights. Biden took a jab at Trump’s recent…

Refinery in Russia engulfed in flames following Ukrainian drone attack

For several months, Russian forces have been targeting energy installations on Ukrainian territory, prompting Kyiv to adopt a similar strategy to slow down supplies to Russian military forces in Ukraine.…

Billie Eilish joins Fortnite update as aggressive emotes removed

Epic Games has released an update for Fortnite (29.30) that includes a new feature allowing players to filter out certain emotes considered “aggressive”. With the v29.30 update, players can choose…